At Global Florida Realty, we’ve noticed a surge of interest in investment properties. Many investors are wondering about current mortgage interest rates on investment properties.

The landscape of real estate investing is constantly shifting, and understanding the factors that influence mortgage rates is key to making informed decisions. This blog post will explore the current state of investment property mortgage rates and provide strategies for securing favorable terms.

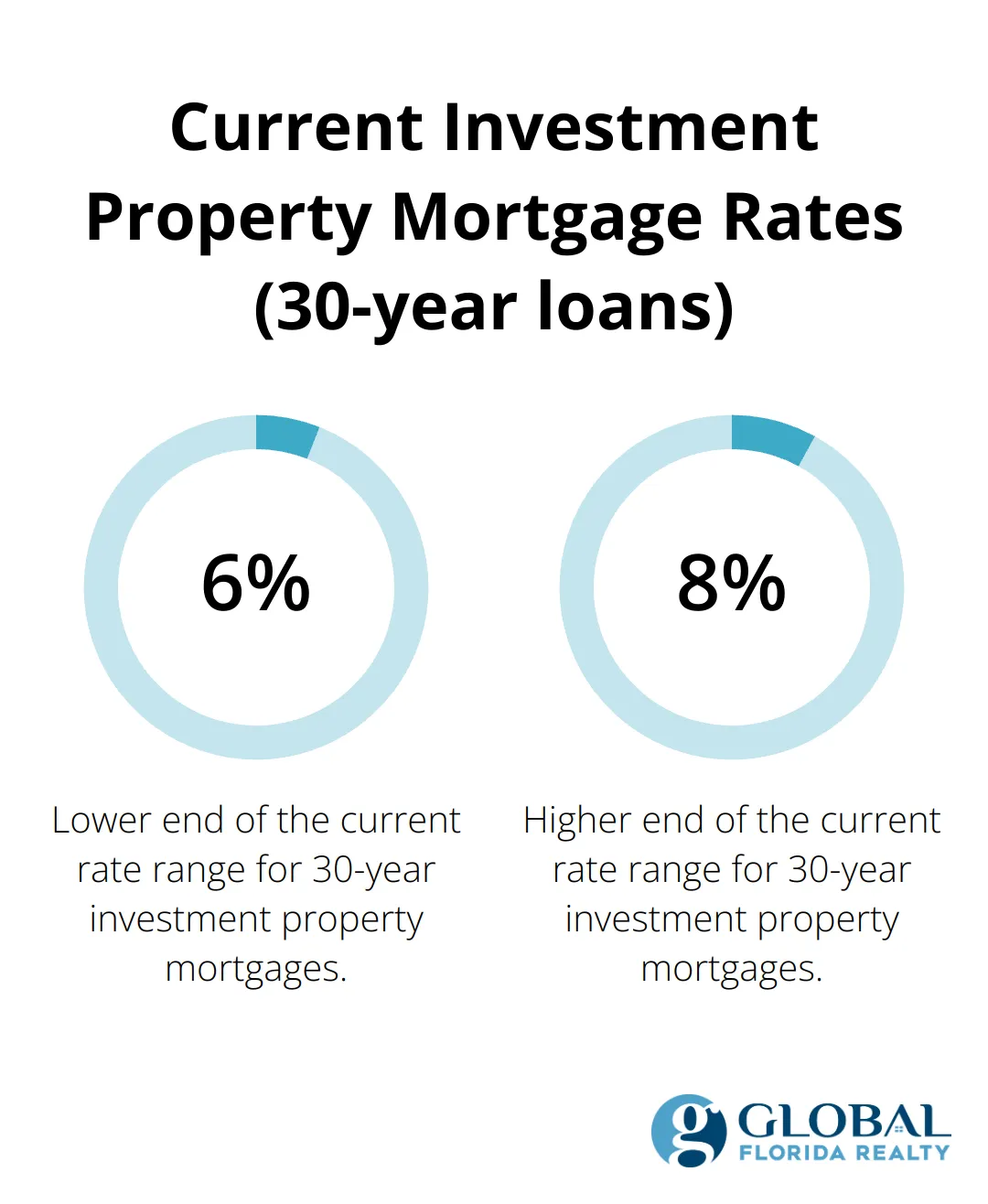

Investment property mortgage rates continue to fluctuate. As of June 11, 2025, 30 year construction-to-permanent loan rates generally fall in the 6.9% to 8.2% range. This exceeds rates for primary residences, which average around 7.20% for conventional loans.

Investment property mortgage rates typically exceed those for primary residences by 0.50% to 0.75%. Lenders impose this premium due to the perceived higher risk associated with investment properties. During financial hardships, borrowers tend to prioritize payments on their primary homes over investment properties.

Several elements shape these rates:

The Federal Reserve’s actions significantly impact mortgage rates. Their recent reduction of the federal funds rate by 1 percentage point in late 2024 has begun to influence the mortgage market. However, investment property rates haven’t decreased as dramatically as some investors anticipated.

Investor activity has slowed recently. Redfin reports that investor home purchases dropped to 17.1% of all home sales in Q4 2024 (the lowest level since 2020). This cooling investor demand could potentially lead to more competitive rates as lenders seek to attract business.

Despite these challenges, real estate remains an attractive investment option. Zillow reports that the average rent for single-family homes reached $2,256 per month in April 2025. This steady rental income potential continues to draw investors to the market, even with higher mortgage rates.

As you navigate the current investment property mortgage landscape, rates can vary significantly between lenders. Shopping around and working with experienced professionals (such as those at Global Florida Realty) can help you secure the most favorable terms in this dynamic market.

The next section will explore the economic factors that drive these investment property mortgage rates, providing a deeper understanding of the market forces at play.

The Federal Reserve’s monetary policy significantly impacts investment property mortgage rates. When the Fed adjusts its federal funds rate, it creates a ripple effect throughout the financial system. Since the three interest rate cuts implemented in late 2024, the benchmark U.S. 10-year Treasury yield has fluctuated modestly but currently remains near 4.50%. However, investment property rates haven’t decreased as dramatically as some investors hoped.

This lag in rate reduction for investment properties stems from lenders’ continued perception of higher risk associated with these loans. Investors should expect investment property rates to remain higher than those for primary residences, even as overall rates trend downward.

Inflation and mortgage rates share a complex relationship that directly affects real estate investors. As inflation rises, lenders typically increase interest rates to maintain their profit margins. This can lead to higher mortgage payments for investors, potentially squeezing profit margins on rental properties.

However, inflation isn’t all bad news for real estate investors. Rising prices often translate to increased rents, which can offset higher mortgage costs.

Investors who secure fixed-rate mortgages during periods of low inflation may find themselves in an advantageous position as inflation rises, effectively reducing the real cost of their debt over time.

The level of investor activity in the real estate market can influence mortgage rates for investment properties. Recent data shows that investor home purchases dropped to 17.1% of all home sales in Q4 2024, the lowest level for Q4 since 2020. This cooling investor demand could potentially lead to more competitive rates as lenders seek to attract business.

However, it’s important to consider regional variations. Some markets, particularly in Florida, continue to see strong investor interest due to factors like population growth and tourism. In these areas, competition for investment properties might remain fierce, potentially keeping rates elevated.

Areas with strong rental markets (such as Orlando with its proximity to major attractions like Disney) continue to attract investor interest despite higher rates. This sustained demand in certain markets underscores the importance of thorough research and local market knowledge when considering investment properties.

Understanding these economic forces proves essential for making informed decisions in the real estate investment market. While higher rates can present challenges, they also create opportunities for investors who can navigate the market effectively. The next section will explore strategies for securing favorable investment property mortgage rates in this dynamic economic environment.

Lenders closely examine your financial health when considering investment property loans. A credit score in the high 600s or 700s can significantly improve your rate offers. To achieve this, pay down existing debts, especially credit card balances. Try to keep your credit utilization ratio below 30%. Also, avoid applying for new credit in the months before your mortgage application.

Your debt-to-income (DTI) ratio is equally important. Lenders prefer a DTI below 43% for investment properties. To lower your DTI, pay off some existing debts or increase your income. This might involve taking on a side job or finding ways to boost your primary income.

Investment properties typically require 15-20% down. However, offering a larger down payment can lead to more favorable rates. Some investors opt for a 25% or even 30% down payment to secure the best possible terms.

A larger down payment reduces the lender’s risk, potentially leading to a rate reduction of 0.25% to 0.5%. This can translate to significant savings over the life of the loan. On a $300,000 loan, a 0.25% rate reduction could save you over $15,000 in interest over 30 years.

Don’t limit yourself to conventional 30-year fixed-rate mortgages. Adjustable-rate mortgages (ARMs) usually offer lower interest rates than fixed-rate mortgages to begin with, which can be advantageous if you plan to sell or refinance within a few years. However, be aware that rates can rise substantially in the future.

Portfolio loans, offered by some banks and credit unions, can provide more flexible terms for investors with multiple properties. These loans are kept on the lender’s books rather than sold on the secondary market, allowing for more customized underwriting.

Working with experienced professionals can make a significant difference in securing favorable rates. Mortgage brokers have access to multiple lenders and can often find better deals than you might on your own. They can also help you navigate the complexities of investment property financing.

Experienced real estate professionals understand the nuances of investment property financing in specific areas. This local expertise can be invaluable, especially in competitive markets like Orlando where investment opportunities abound.

Begin improving your financial profile well in advance of your property search. Stay informed about market trends and economic factors that influence mortgage rates. This knowledge will help you make timely decisions and potentially secure better rates.

Investment property mortgage rates exceed those for primary residences, reflecting lenders’ risk perception. Current mortgage interest rates on investment properties range from 6.9% to 8.2% for 30-year loans, about 0.5% to 0.75% above primary residence rates. These rates respond to Federal Reserve policies, inflation, and market demand, with potential for gradual stabilization as the market adjusts to recent economic shifts.

Investors should prepare for continued rate volatility. The cooling investor demand observed in late 2024 might lead to more competitive rates. However, strong rental markets in areas like Florida may keep rates elevated due to sustained investor interest.

We at Global Florida Realty understand the complexities of investment property financing. Our team specializes in desirable areas like Orlando, assisting with both personal homes and investment properties (including vacation rentals near major attractions). We provide guidance on effective home marketing, property valuations, and management for short-term and long-term leasing.