At Global Florida Realty, we often encounter investors curious about the intricacies of real estate financing. One common question we hear is, “What is underwriting in real estate investing?”

Underwriting is a critical process that determines the viability and risk of a real estate investment. It involves a thorough analysis of various factors, including property value, market conditions, and the borrower’s financial health.

Real estate underwriting forms the backbone of sound investment decisions. This meticulous process involves a comprehensive evaluation of a property’s financial viability and associated risks. Underwriting determines the potential profitability and risk level of a real estate investment, making it essential for both investors and lenders.

Underwriting in real estate investing transcends basic calculations. It adopts a multi-faceted approach that considers various factors:

Underwriters also scrutinize the borrower’s financial health, including credit history, income stability, and debt-to-income ratio.

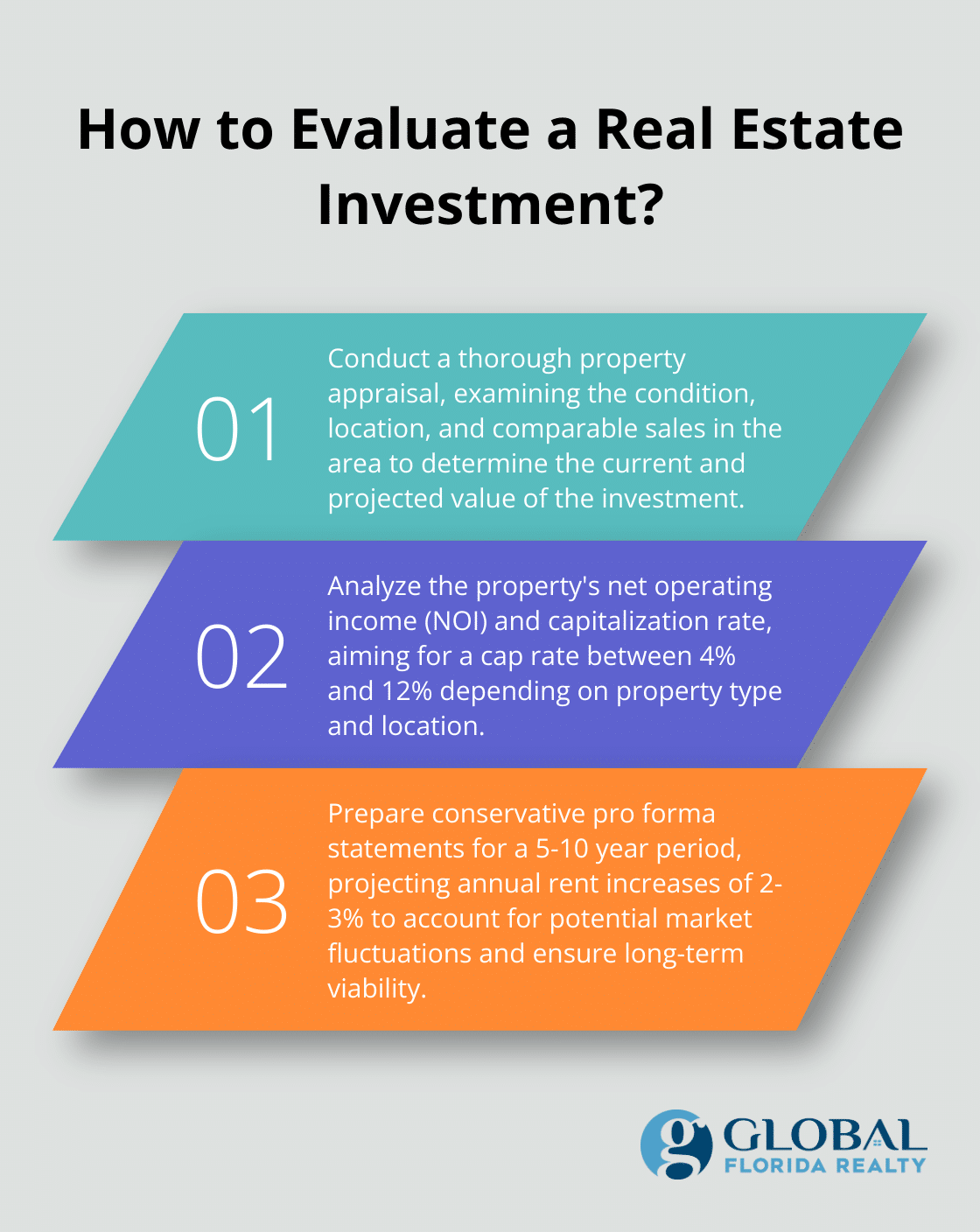

A primary component of underwriting is the property appraisal. This assessment examines the property’s condition, location, and comparable sales in the area. The National Association of Realtors has conducted surveys to determine the impact of appraisals on the current market and member business in terms of cost, turn-around times, and other challenges.

Another critical aspect involves the analysis of income and expenses. For investment properties, underwriters typically examine the property’s net operating income (NOI) and capitalization rate. The Urban Land Institute indicates that a healthy cap rate for most commercial properties ranges between 4% and 12% (varying based on property type and location).

For investors, thorough underwriting distinguishes between a profitable venture and a financial pitfall. It provides a clear picture of the investment’s potential returns and associated risks. Recent research has delved into the intricate dynamics of Core and Non-Core private equity real estate strategies in response to turbulent times.

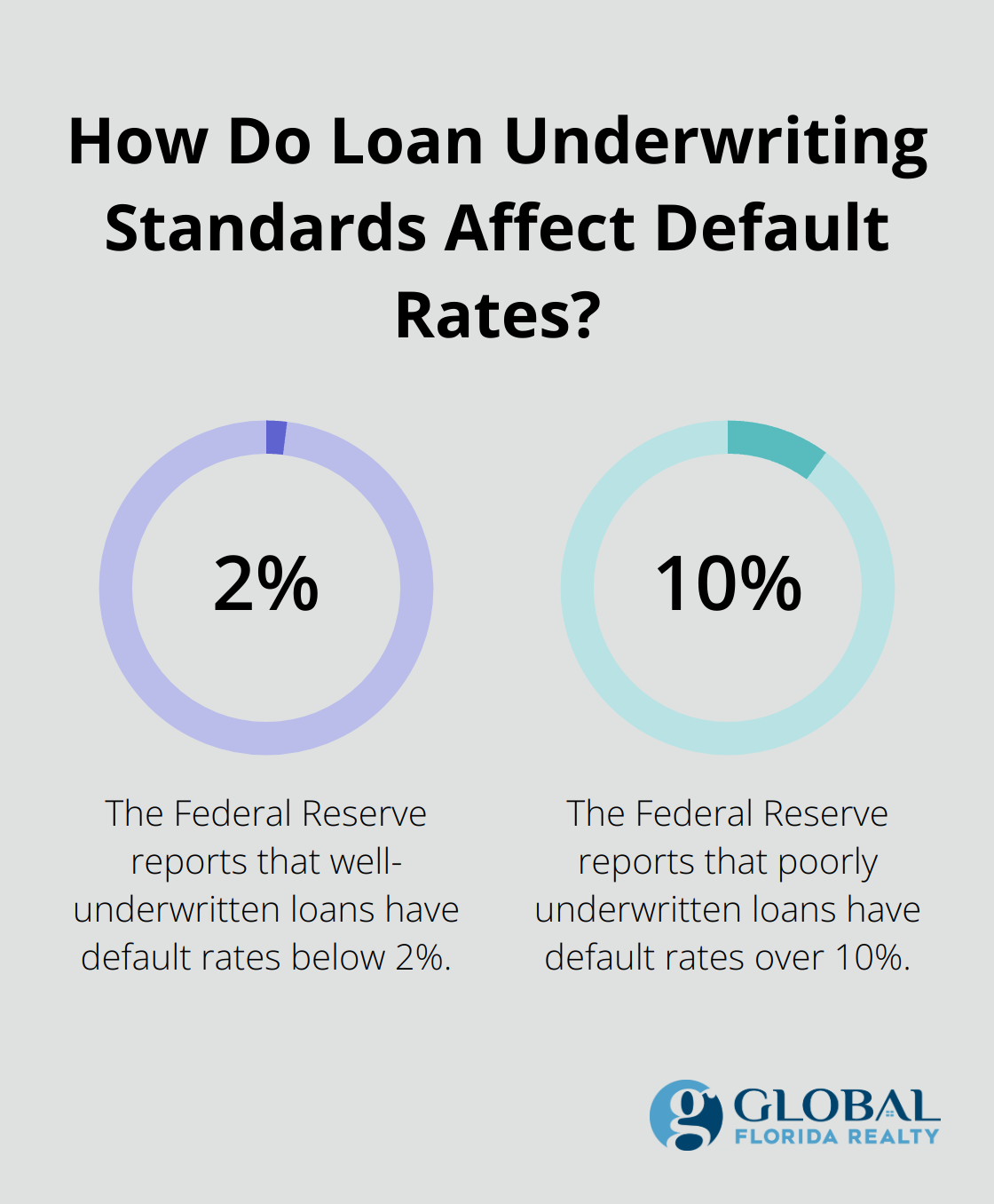

Lenders rely on underwriting to assess the risk of default and determine appropriate loan terms. The Federal Reserve reports that well-underwritten loans have default rates below 2%, compared to over 10% for poorly underwritten ones.

Top real estate firms employ industry-leading underwriting practices to ensure their clients make informed decisions. These firms analyze everything from local market trends to property-specific financials, providing a comprehensive risk assessment that goes beyond surface-level evaluations.

As we move forward, we’ll explore the specific factors that underwriters analyze in detail during the real estate underwriting process.

Real estate underwriting involves a thorough examination of various aspects of a potential investment. This process determines the viability and risk associated with a property. Let’s explore the key factors that underwriters analyze to assess real estate investments.

Underwriters begin by evaluating the property’s current market value. They compare the property to similar ones in the area, considering factors like location, size, and condition. The nationwide median sale price for existing homes in August clocked in at $416,700. This data helps underwriters determine if the property’s asking price aligns with market trends.

Market analysis extends beyond the property itself. Underwriters examine local economic indicators, population growth, and employment rates. For example, Orlando’s population grew by 1.8% between 2021 and 2022 (outpacing the national average). Such growth can indicate a strong rental market, which is important for investment properties.

For investment properties, underwriters analyze potential income and expenses meticulously. They examine current rental rates in the area and project future income based on market trends. The Urban Land Institute reported that in 2023, the average apartment rent growth in the U.S. was 2.6%.

On the expense side, underwriters consider property taxes, insurance, maintenance costs, and potential vacancies. They typically use a vacancy rate of 5-10% in their calculations (depending on local market conditions). These projections help determine the property’s net operating income (NOI) and capitalization rate, which are essential metrics for investment decisions.

Underwriters act as risk managers. They identify potential risks associated with the property and develop strategies to mitigate them. This might include environmental assessments, especially in areas prone to natural disasters. Properties in Florida often require additional insurance for hurricane protection, which can significantly impact the overall investment cost.

Another risk factor is the property’s condition. Underwriters may require a professional inspection to identify any major repairs or upgrades needed. They factor these costs into their analysis to ensure the investment remains profitable.

The final piece of the underwriting puzzle is the borrower’s financial situation. Underwriters scrutinize credit scores, income stability, and debt-to-income ratios. FHA loan applicants must have a minimum FICO® score of 580 to qualify for the low down payment advantage which is currently at 3.5%. However, conventional loans often require higher scores, usually 620 or above.

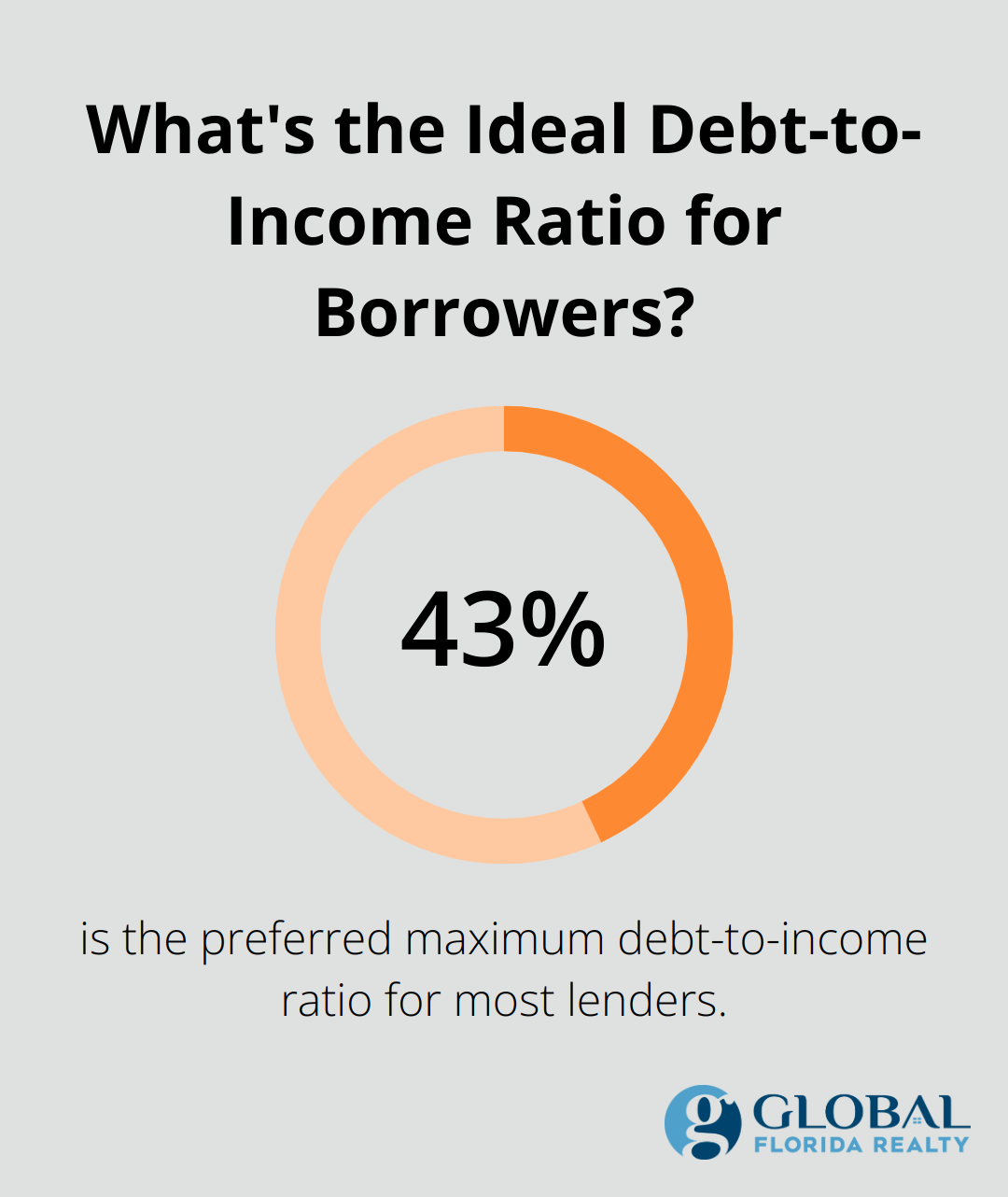

Debt-to-income ratio is another critical factor. Most lenders prefer a ratio of 43% or lower, meaning total monthly debt payments shouldn’t exceed 43% of gross monthly income. This ensures that borrowers have sufficient income to cover their mortgage payments and other financial obligations.

As we move forward, we’ll explore the step-by-step process that underwriters follow to gather and analyze this information, creating a comprehensive picture of the investment opportunity.

The underwriting process in real estate investing requires attention to detail and a systematic approach. This critical stage can significantly impact the success of an investment. Let’s explore the key steps involved in this process.

The underwriting process begins with the collection of a comprehensive set of documents. These typically include:

Financial statements (past 2-3 years)

Tax returns (personal and business)

Rent rolls and lease agreements

Property operating statements

Bank statements

Credit reports

For investment properties, underwriters often require additional documents such as property management reports and capital expenditure histories. Data are readily available for transactions in excess of $2.5 million from several sources, including Real Capital Analytics (RCA).

After the collection of necessary documents, underwriters perform a detailed financial analysis. This step involves the scrutiny of income streams, evaluation of expenses, and assessment of the property’s overall financial health.

Underwriters use industry-standard metrics like the debt service coverage ratio (DSCR) to evaluate a property’s ability to generate sufficient income to cover debt obligations. Most lenders consider a DSCR of 1.25 or higher favorable.

Pro forma statements are forward-looking financial projections that estimate a property’s future performance. These statements typically cover a 5-10 year period and include projected income, expenses, and cash flows.

Underwriters often use conservative estimates when they create pro forma statements to account for potential market fluctuations. For example, they might project annual rent increases of 2-3% (even if the current market shows higher growth rates). This conservative approach helps ensure that the investment remains viable even in less favorable market conditions.

The underwriting process culminates in the determination of loan terms. Based on the conducted analysis, underwriters decide on key loan parameters such as:

Loan-to-Value (LTV) ratio

Interest rate

Loan term

Prepayment penalties

A good LTV ratio should be no greater than 80%. Anything above 80% is considered to be a high LTV, which means that borrowers may face higher interest rates or additional requirements.

Clear and timely communication between the lender, borrower, and real estate professionals can significantly expedite the underwriting process. This efficient communication potentially reduces the time from application to approval by 20-30%.

The underwriting process provides a comprehensive view of the investment opportunity. It helps to ensure that all parties enter into the transaction with a clear understanding of the risks and potential rewards.

Underwriting in real estate investing forms the foundation of sound investment decisions. It evaluates a property’s financial viability, market conditions, and associated risks. Thorough analysis of property valuation, income projections, and borrower creditworthiness helps investors and lenders make informed decisions.

We at Global Florida Realty understand the importance of underwriting in real estate investing. Our comprehensive services include guidance through every step of the investment process, including underwriting. We assist clients in buying, selling, and investing in desirable areas like Orlando.

Real estate investors should prioritize underwriting in their decision-making process. It minimizes risks, maximizes returns, and builds robust real estate portfolios. Successful real estate investing requires understanding a property’s true value and potential through rigorous underwriting (a skill that separates profitable ventures from potential financial pitfalls).