Florida real estate contract contingencies play a vital role in protecting both buyers and sellers during property transactions. These clauses provide essential safeguards and outline specific conditions that must be met for a deal to proceed.

At Global Florida Realty, we understand the importance of these contingencies in ensuring smooth and fair real estate transactions. This blog post will explore three key contingencies: financing, inspection, and appraisal, helping you navigate the complexities of Florida’s real estate market with confidence.

A financing contingency is a key protection in Florida real estate contracts. This clause allows buyers to withdraw from a deal without penalty if they fail to secure a mortgage loan. At Global Florida Realty, we recognize the importance of this safeguard in preventing buyers from financial overextension.

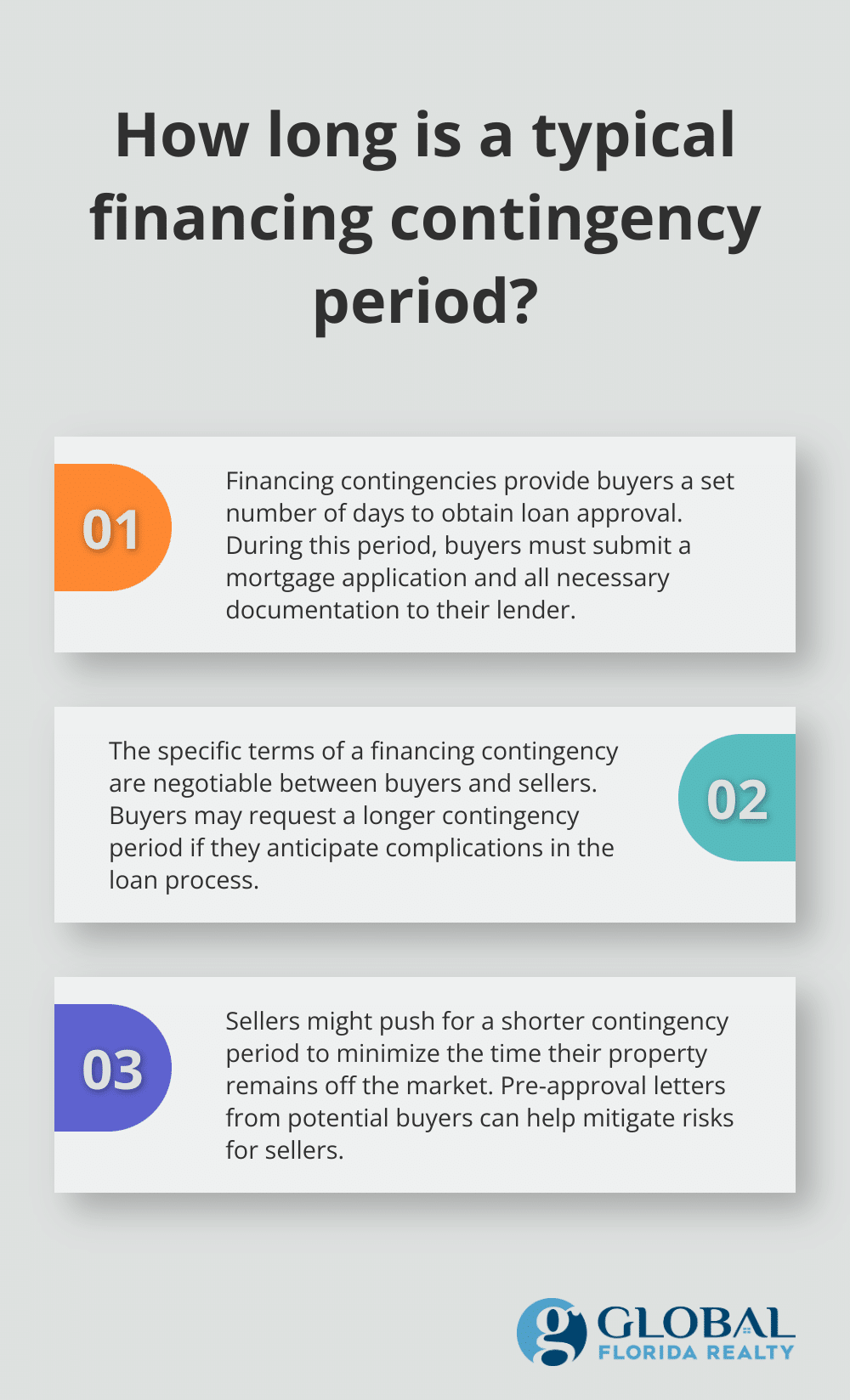

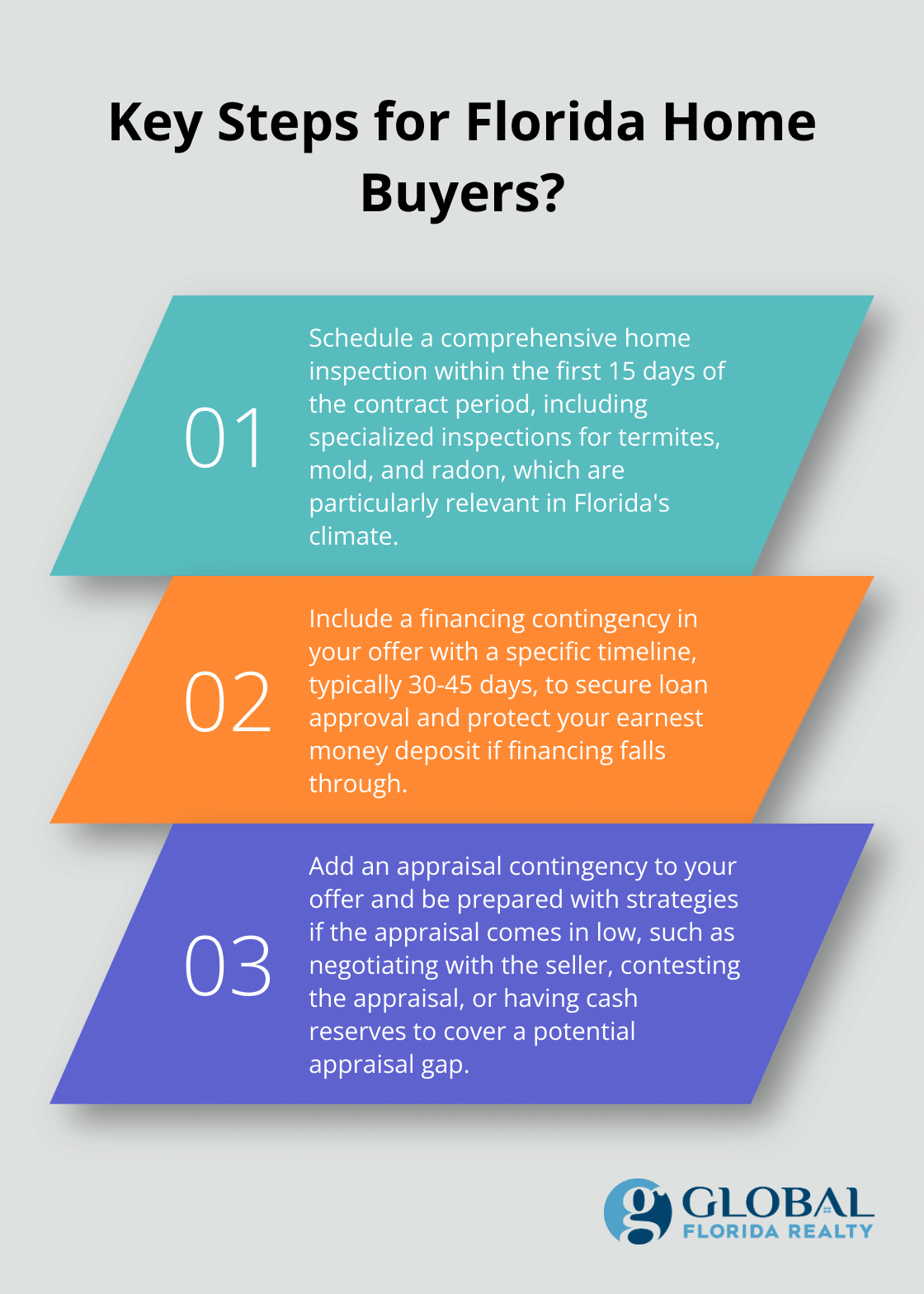

Financing contingencies typically provide buyers with a set number of days to obtain loan approval. During this period, buyers must submit a mortgage application and provide all necessary documentation to their lender. If the loan doesn’t receive approval within the specified timeframe, buyers can cancel the contract and reclaim their earnest money deposit.

The primary benefit for buyers is obvious: protection against a legal obligation to purchase a home they can’t afford. Sellers also gain advantages. By establishing a clear timeline, they avoid indefinite property entanglement while a buyer attempts to secure financing.

Financing contingencies, while generally favorable to buyers, can present risks for sellers. To address these concerns, we often advise sellers to request a pre-approval letter from potential buyers. This document (although not a guarantee) indicates that a lender has reviewed the buyer’s financial situation and will likely approve a loan.

The specific terms of a financing contingency are open to negotiation. Buyers might request a longer contingency period if they anticipate complications in the loan process. Conversely, sellers might push for a shorter period to minimize the time their property remains off the market.

In competitive markets, some buyers consider waiving the financing contingency to enhance their offer’s attractiveness. However, this approach carries significant risks, and we generally don’t recommend it unless the buyer has absolute certainty about their financial situation.

As we move forward, it’s important to understand that financing contingencies represent just one aspect of the complex world of real estate contracts. The next critical element we’ll explore is the inspection contingency, which plays an equally vital role in protecting buyers’ interests.

Home inspections form a critical part of real estate transactions in Florida. An inspection contingency in a purchase agreement allows buyers to have the property professionally examined. This clause empowers buyers to renegotiate or withdraw from the deal based on the inspection findings.

A standard home inspection typically covers the structure, foundation, roof, electrical systems, plumbing, and HVAC. However, Florida’s unique climate and geography often necessitate additional specialized inspections:

Standard home inspection prices in Florida typically range from $250 to $400, depending on the square footage of your home and other factors.

After receiving the inspection report, buyers typically have three main options:

The contract usually specifies a timeframe of 15 days after the inspection for these decisions.

If the inspection uncovers issues, buyers can request that sellers make repairs or offer credits at closing. Buyers should prioritize major issues that affect safety or functionality, such as roof leaks, electrical problems, or HVAC failures.

For instance, if an inspection reveals that a home’s air conditioning system nears the end of its lifespan, a buyer might request a $5,000 credit towards future replacement rather than asking the seller to install a new system before closing.

Sellers are not obligated to make repairs or offer credits. In some cases (especially in a seller’s market), buyers may need to weigh the cost of potential repairs against the risk of losing the property if they push too hard in negotiations.

Many sellers in Florida use “As-Is” contracts, which still allow for an inspection period but don’t obligate the seller to make any repairs. In these cases, buyers must decide whether to accept the property’s condition or walk away from the deal.

The Florida Realtors Association reports that approximately 60% of residential real estate contracts in the state use the “As-Is” format. This trend underscores the importance of thorough inspections and careful consideration of potential repair costs before committing to a purchase.

As we move from inspection contingencies to appraisal contingencies, it’s important to understand how property valuation can impact your real estate transaction. Let’s explore how appraisal contingencies protect buyers and what options exist when appraisals come in lower than expected.

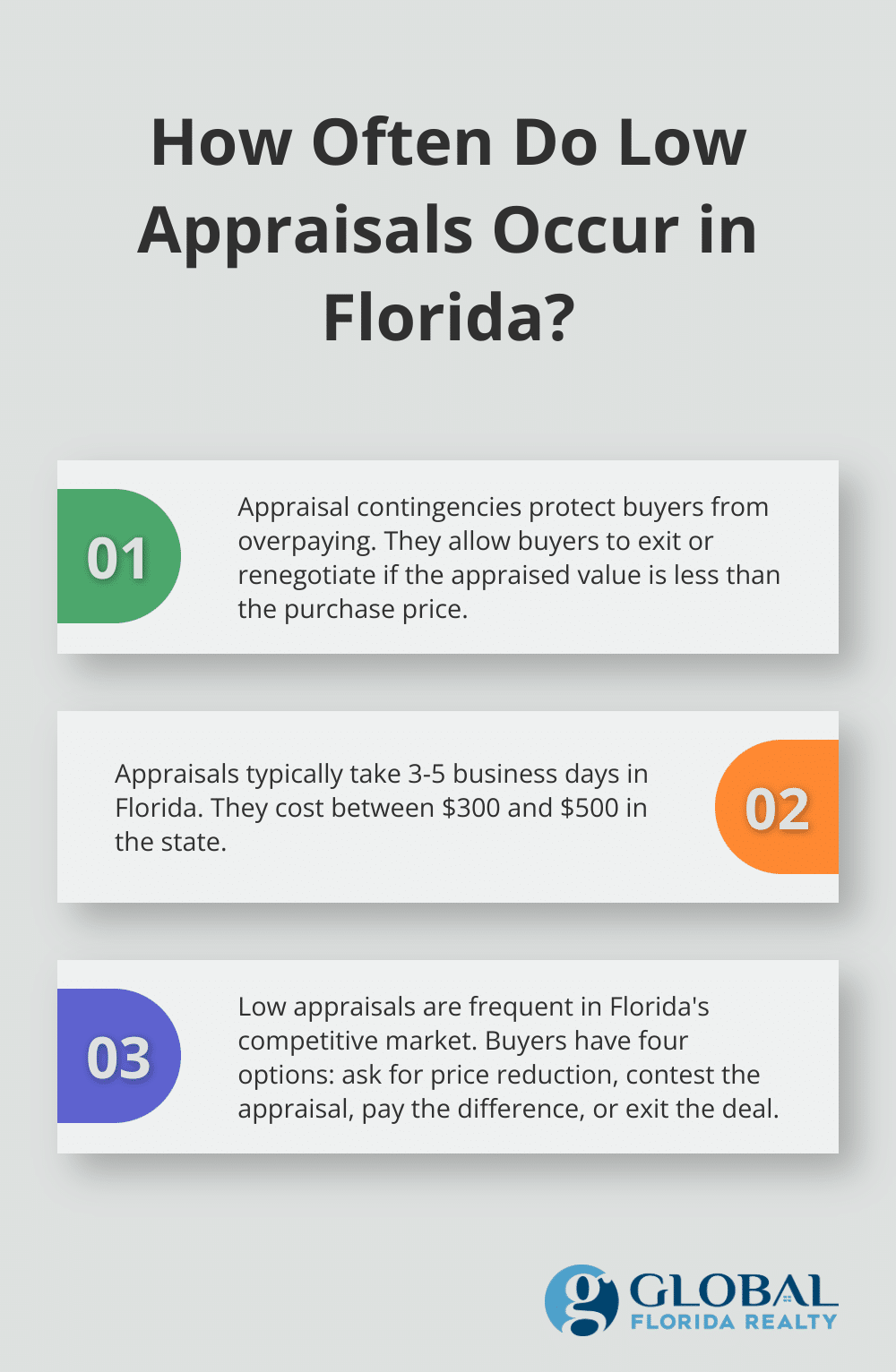

Appraisal contingencies form a key part of Florida real estate transactions. They protect buyers from paying too much for properties. This clause allows buyers to exit a deal or negotiate if the property’s appraised value is less than the agreed purchase price.

When a buyer applies for a mortgage, the lender usually requires an appraisal. This ensures the property’s value justifies the loan amount. A licensed appraiser evaluates the home, considering factors like location, condition, and recent sales of similar properties. The process typically takes 3-5 business days and costs between $300 and $500 in Florida.

Appraisal contingencies provide valuable protection in Florida’s dynamic real estate market. If a property appraises for less than the purchase price, the buyer isn’t required to proceed with the transaction. This protection is essential, as lenders generally won’t approve a mortgage for more than the appraised value.

For instance, if you agree to buy a home for $300,000, but it appraises for only $280,000, your lender will likely cap their loan at $280,000. Without an appraisal contingency, you’d need to cover the $20,000 difference or risk losing your earnest money deposit.

Low appraisals occur frequently in Florida’s competitive market. The National Association of Realtors reports on appraisal issues affecting the current market and member business.

When faced with a low appraisal, buyers typically have four options:

Buyers should include an appraisal contingency in their offer, especially in hot markets where bidding wars can drive prices above market value. Don’t waive this contingency unless you’re ready to cover any appraisal gap out of pocket.

Sellers should prepare for potential appraisal issues. Consider getting a pre-listing appraisal to price your home accurately. If an appraisal comes in low, be open to negotiation, especially if comparable sales support the appraised value.

We’ve seen cases where sellers have successfully challenged low appraisals by providing additional information about recent upgrades or unique features (that may have been overlooked). In one instance, a seller in Orlando increased the appraised value by $15,000 by highlighting recent energy-efficient improvements.

Understanding and effectively using appraisal contingencies can make the difference between a smooth transaction and a costly mistake in Florida’s real estate market.

Florida real estate contract contingencies protect buyers and sellers during property transactions. These contingencies include financing, inspection, and appraisal clauses, each serving a unique purpose in safeguarding the interests of all parties involved. Understanding these contingencies is essential for anyone who wants to navigate the Florida real estate market successfully.

The complexities of these clauses can challenge individuals without expert guidance. At Global Florida Realty, we offer our expertise to help clients understand and use these contingencies effectively. Our team specializes in Florida’s diverse real estate market, providing comprehensive services for buying, selling, and investing.

Working with a knowledgeable real estate professional is invaluable when dealing with Florida real estate contract contingencies. They can help you navigate the intricacies of these clauses, ensuring that your interests are protected and your goals are achieved. With the right guidance, you can make informed decisions that align with your long-term objectives in the Florida real estate market.