Retiring comfortably is a goal many of us share, and rental properties can be a powerful tool to achieve it. At Global Florida Realty, we often get asked how many rental properties are needed to retire. The answer isn’t one-size-fits-all, as it depends on various factors like your lifestyle, retirement goals, and expected expenses.

In this post, we’ll explore the key considerations and strategies to help you determine the right number of rental properties for your retirement plan.

Your current lifestyle and future retirement goals significantly influence the number of rental properties you’ll need. Start by outlining your desired retirement lifestyle. This includes estimating daily living expenses, travel plans, healthcare costs, and any other activities you wish to pursue. A retiree who plans a modest lifestyle in a small town will need fewer rental properties than someone planning extensive travel or residing in a high-cost area.

The income generated from your rental properties isn’t just about the rent you collect. You must account for various expenses that reduce your profits. These typically include property taxes, insurance, maintenance, and potential property management fees. Total revenue, measured as a percent of Gross Potential Rent (GPR), fell nearly 200 basis points from the prior year while operating expenses increased. Analyze potential properties to ensure you select options with favorable income-to-expense ratios.

Inflation can significantly impact your retirement plans. Historically, the U.S. inflation rate has averaged around 3% annually. This means the purchasing power of your rental income will decrease over time if rents don’t keep pace with inflation. When planning your retirement portfolio, factor in regular rent increases and choose properties in areas with strong economic growth potential to help combat inflation’s effects.

No rental property guarantees 100% occupancy. Vacancies are a reality that can dramatically affect your income. The homeowner vacancy rate declined 0.6 percentage points between the fourth quarter of 2019 and the first quarter of 2022, from 1.4% to 0.8%. Market fluctuations can also impact rent prices and property values. Diversify your portfolio across different locations and property types to help mitigate these risks.

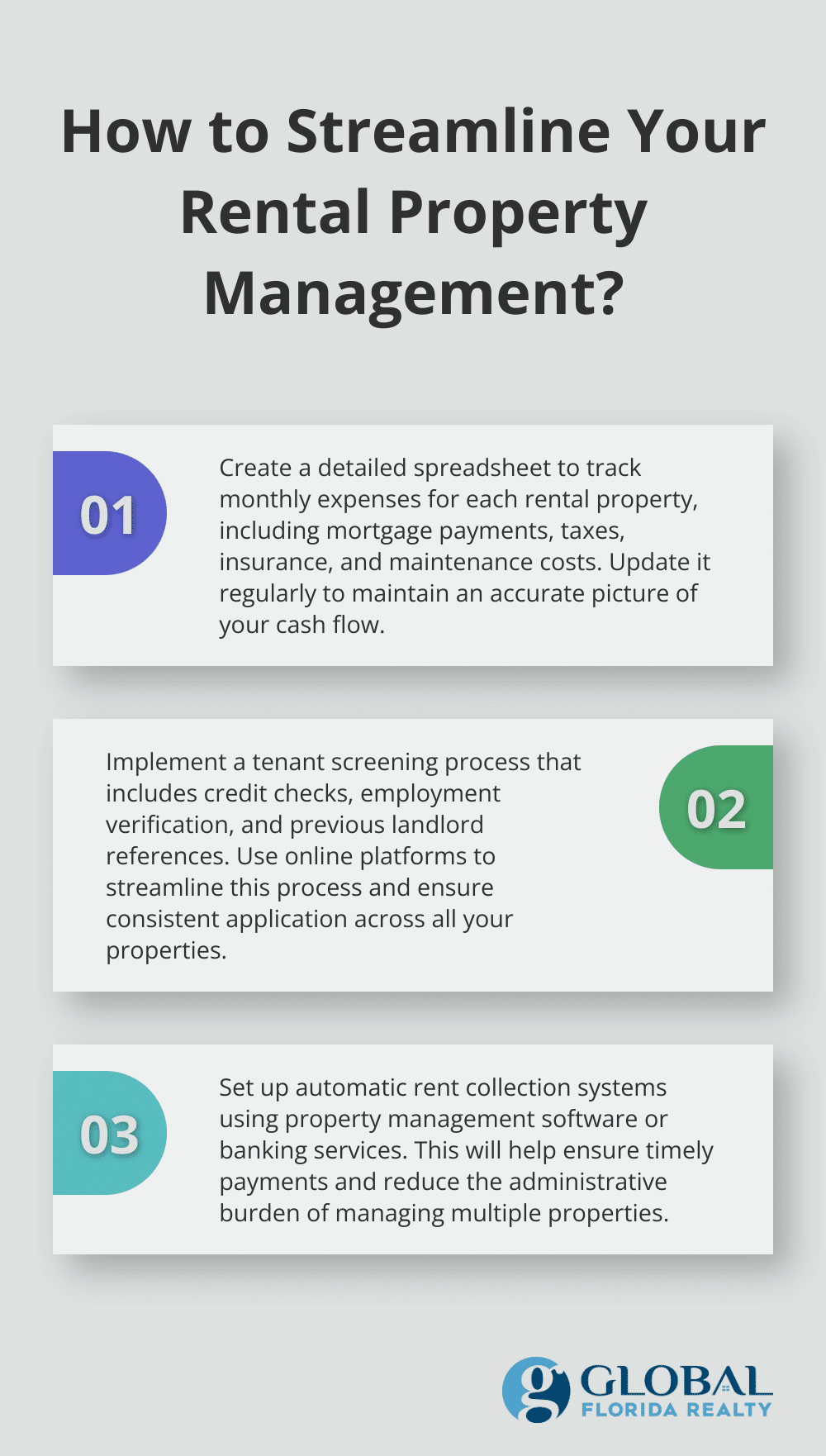

Effective property management plays a vital role in maximizing your rental income. You have two main options: self-management or hiring a professional property management company. Self-management can save money but requires significant time and effort. Professional management (which typically costs 8-12% of monthly rent) can handle tenant screening, maintenance, and rent collection, allowing for a more hands-off approach. Your choice will impact your overall returns and the number of properties you can effectively manage.

As you consider these factors, it’s essential to calculate your specific retirement needs accurately. Let’s explore how to determine the exact number of rental properties required to fund your retirement comfortably.

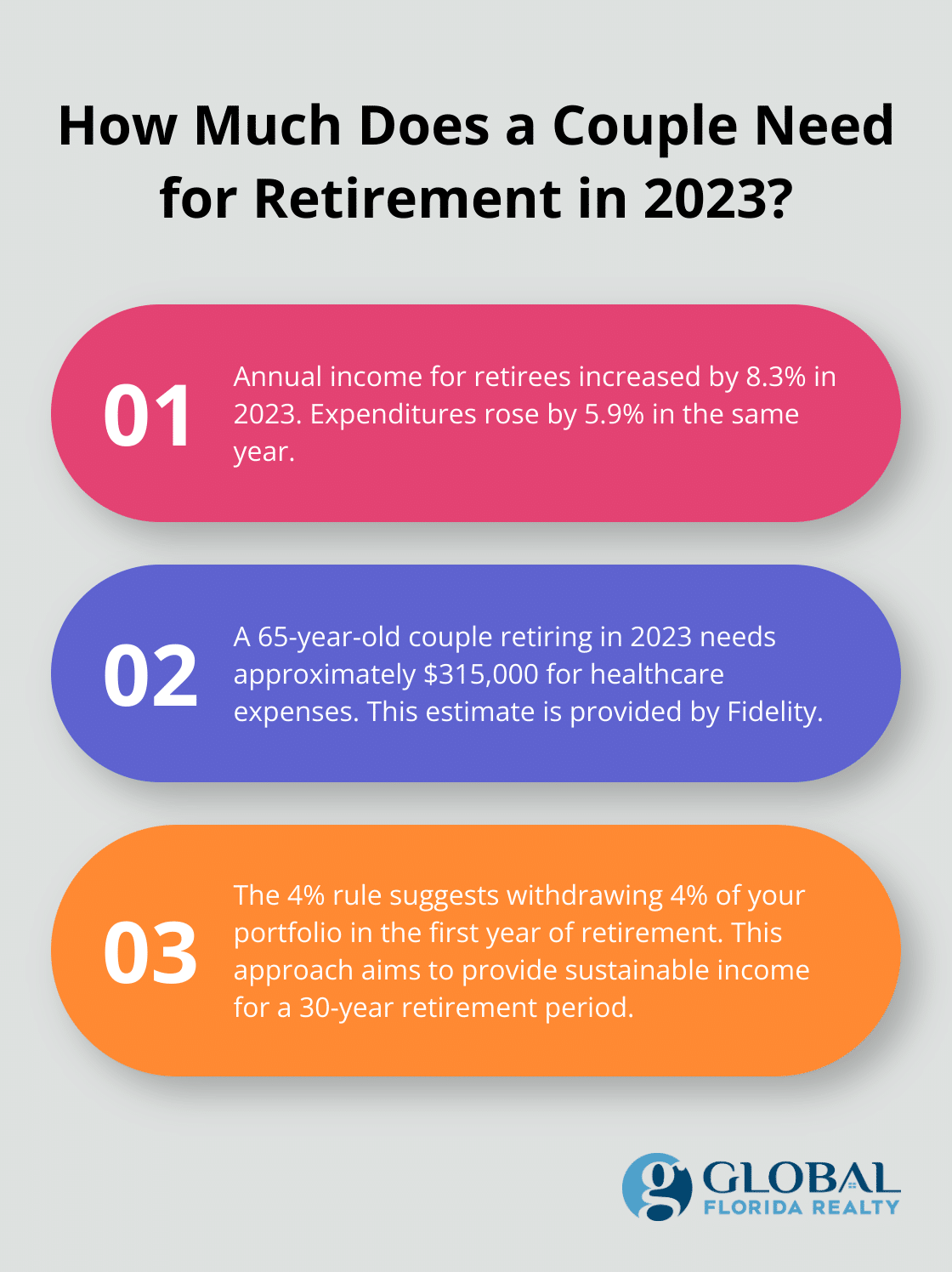

To determine the number of rental properties needed for retirement, you must first calculate your expected monthly expenses. While specific figures may vary based on your lifestyle and location, it’s important to consider overall trends in retiree spending. Recent data from the Bureau of Labor Statistics shows that both income and expenditures for retirees have increased, with annual income before taxes rising 8.3 percent in 2023, while expenditures increased 5.9 percent. Don’t overlook healthcare costs, which increase with age. Fidelity estimates that a 65-year-old couple retiring in 2023 will need approximately $315,000 saved for healthcare expenses in retirement.

After estimating your monthly expenses, subtract any guaranteed income sources (such as Social Security or pensions). The remaining amount represents what you’ll need to generate from your rental properties and other investments. For example, if you need $5,000 per month and expect $2,000 from Social Security, you’ll need to generate $3,000 from your rental portfolio.

Diversification strengthens retirement income stability. While rental properties provide steady cash flow, consider other income sources. These might include 401(k)s, IRAs, stocks, or bonds. Each has different tax implications and withdrawal strategies, so consult with a financial advisor to optimize your retirement income mix.

The 4% rule serves as a common guideline in retirement planning. It suggests that you can withdraw 4% of your portfolio in the first year of retirement, then adjust that amount for inflation each subsequent year. This approach offers a high probability of not outliving your savings over a 30-year retirement, but may not provide sustainable income for individuals who retire early.

For rental properties, try to achieve a cash-on-cash return of at least 4% annually. This means if you invest $1,000,000 in rental properties, you should aim to generate at least $40,000 in annual cash flow after all expenses. Many real estate investors target higher returns, often in the 6-8% range or more.

These calculations provide a starting point for your retirement planning. Your specific needs may vary based on factors like health, lifestyle choices, and unexpected expenses. Regular review and adjustment of your retirement plan will help you stay on track as your circumstances change.

Now that you understand how to calculate your retirement income needs, let’s explore strategies to build a profitable rental portfolio that can support your retirement goals.

The real estate mantra “location, location, location” remains true for investment properties. We focus on areas with robust economic indicators, job growth, and population increases. Orlando, for example, has experienced a 1.8% population growth rate and a 3.3% job growth rate in recent years, making it an attractive market for rental properties. You should search for neighborhoods with quality schools, low crime rates, and easy access to amenities. These factors contribute to higher property values and rental demand over time.

When choosing properties, you should prioritize those with positive cash flow potential. Look for properties where the monthly rent can cover mortgage payments, taxes, insurance, and maintenance costs while still providing a profit. The 1% rule serves as a helpful guideline: monthly rent should be at least 1% of the property’s purchase price to ensure profit.

Consider properties that need minimal renovations to become rent-ready. While fixer-uppers can offer good deals, they often come with unexpected costs and delays. You should balance potential returns with the time and money needed for improvements.

Leverage can significantly boost your returns when used wisely. You should explore different financing options to expand your portfolio faster. Conventional mortgages typically require 20-25% down for investment properties. However, FHA loans allow for lower down payments on multi-unit properties if you plan to live in one unit.

You can consider using cash-out refinancing on existing properties to fund new purchases. This strategy allows you to tap into built-up equity without selling your current investments. Each financing decision impacts your cash flow and long-term profitability, so you should weigh the costs and benefits carefully.

Proper management maximizes returns and minimizes headaches. You should implement a thorough tenant screening process to reduce the risk of late payments or property damage. According to TransUnion, 91% of property managers report rent payments to help residents build their credit scores, followed by 70% who do so to encourage on-time payments.

Regular property inspections and prompt maintenance address small issues before they become costly problems. You can use property management software to streamline operations. These tools can help with rent collection, maintenance requests, and financial tracking.

For those with multiple properties or limited time, professional property management might be worth the cost. While fees typically range from 8-12% of monthly rent, good managers can increase occupancy rates and handle time-consuming tasks, allowing you to focus on portfolio growth. If you decide to use a property management company, Global Florida Realty offers comprehensive services that can help maximize your investment returns.

The number of rental properties needed to retire comfortably varies for each individual. Your lifestyle, retirement goals, and expected rental income all influence this calculation. You can create a personalized retirement plan by estimating monthly expenses, considering other income sources, and applying strategies like the 4% rule.

A profitable rental portfolio requires strategic thinking and informed decisions. You should select properties in promising locations, maximize cash flow, use financing options wisely, and implement effective management techniques. These steps will help create a sustainable retirement income stream from real estate investments.

We at Global Florida Realty can help you start or expand your rental portfolio. Our team offers comprehensive services to ensure your investment aligns with your retirement goals. Visit our website to learn more about how we can assist you in creating a robust rental property portfolio for a secure retirement.