At Global Florida Realty, we often field questions about rental property income and its tax implications. Many property owners wonder: Do rental properties count as income? The answer is yes, and understanding how to report this income correctly is vital for tax compliance. This blog post will guide you through the essentials of rental income taxation, helping you navigate the complexities of property investment with confidence.

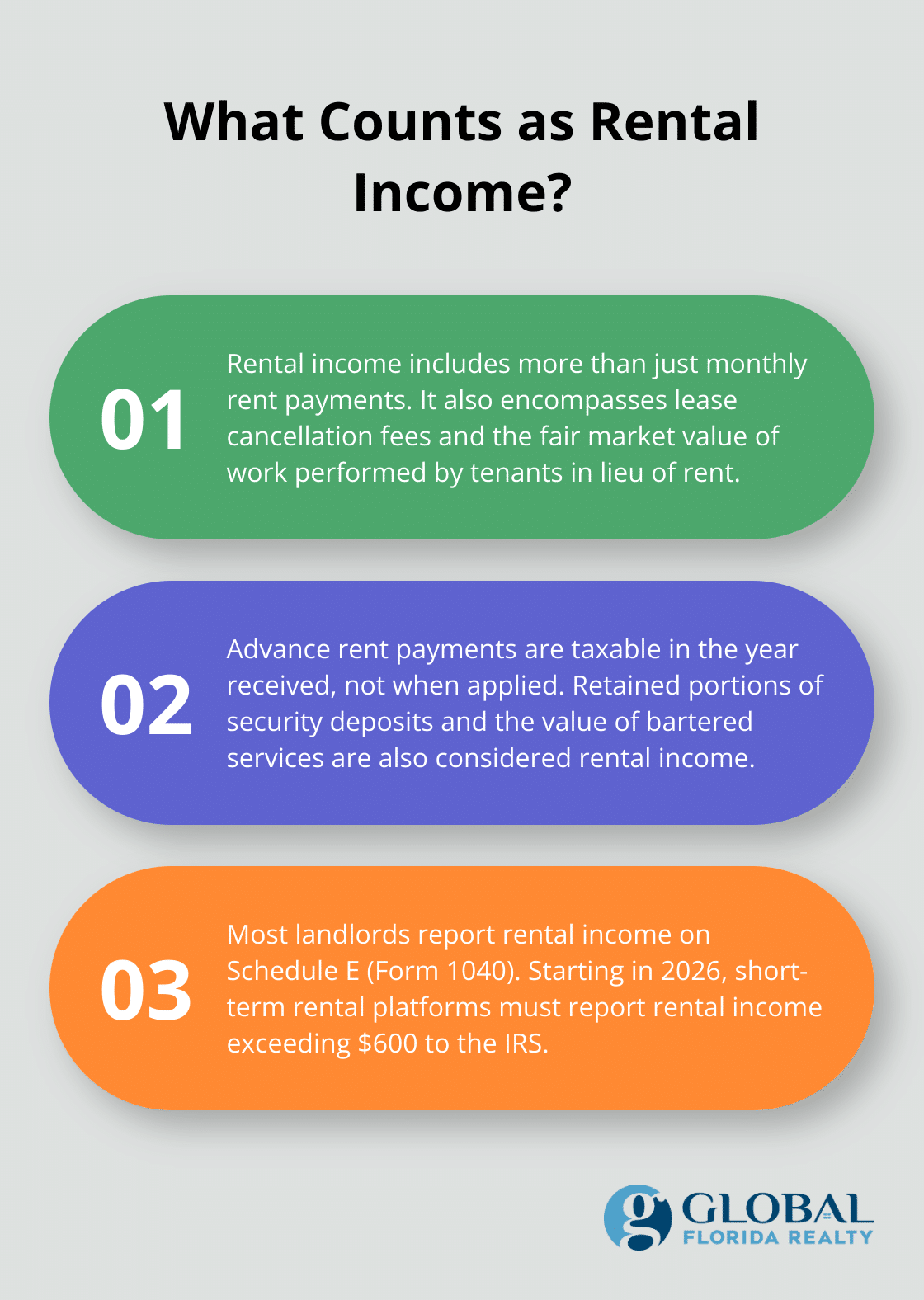

The IRS defines rental income more extensively than many property owners realize. It’s not just the monthly checks from tenants. At Global Florida Realty, we often clarify this misconception for our clients.

Rental income encompasses any payment received for property use or occupation. This includes:

Some rental income sources catch property owners off guard:

The IRS mandates reporting of all rental income on tax returns. Most landlords use Schedule E (Form 1040). However, Schedule C might be necessary if you provide substantial tenant services (e.g., regular cleaning or linen changes).

Meticulous record-keeping is essential (especially with the IRS’s increased focus on rental income). Starting in 2026, short-term rental platforms must report rental income exceeding $600 to the IRS, making precise reporting more critical than ever.

While rental income might seem straightforward, its tax implications often prove more nuanced. Understanding what counts as rental income forms the foundation for tax compliance and investment optimization.

As we move forward, let’s examine how to report this income correctly on your tax return, ensuring you maximize deductions while staying compliant with IRS guidelines.

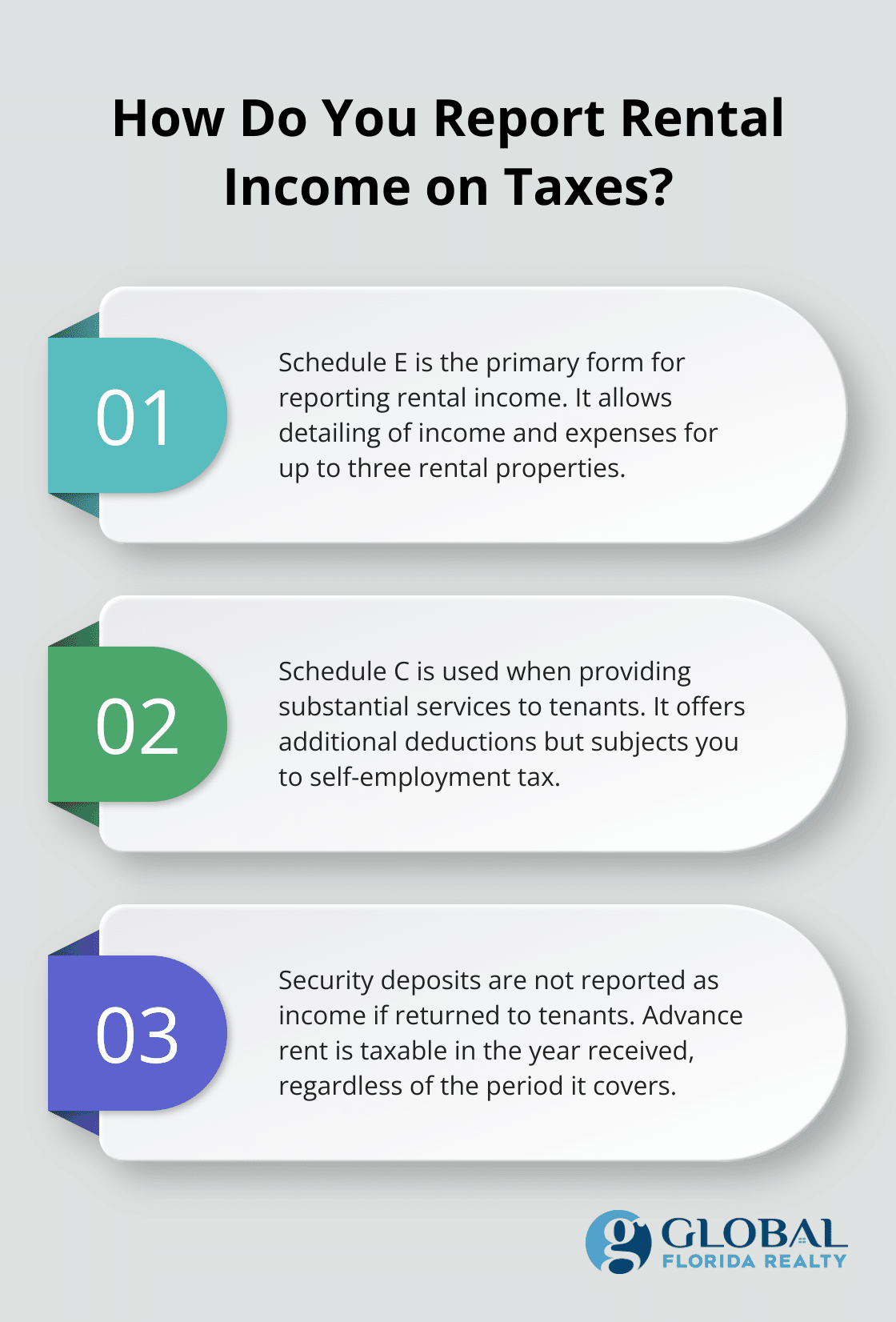

Schedule E (Form 1040) serves as the primary form for reporting income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests. This form allows property owners to detail income and expenses for up to three rental properties. Owners with more than three properties must attach additional Schedule E forms.

On Schedule E, you report all rental income received during the tax year. This includes monthly rent payments, advance rent, retained security deposits, and the fair market value of property or services received as rent.

While Schedule E is common for most rental property owners, certain situations call for Schedule C (Form 1040). If you provide substantial services to tenants, the IRS may consider your rental activity a business rather than a passive investment.

Schedule C can offer advantages, allowing for additional deductions related to self-employment. However, it also subjects you to self-employment tax. A tax professional can help determine which form best suits your situation.

Security deposits and advance rent require special attention in rental income reporting. Don’t include security deposits as income if you plan to return them at the end of the lease. However, any portion of the deposit you keep due to lease violations or damages becomes taxable in the year you decide to retain it.

Advance rent is always taxable in the year received, regardless of the period it covers. For example, if a tenant pays first and last month’s rent upon moving in, you must report both payments as income in the current tax year (even if the last month’s rent won’t apply until the following year).

Accurate reporting of rental income extends beyond mere compliance; it’s a cornerstone of smart financial management. Understanding these nuances allows for better planning of tax obligations and more informed decisions about rental property investments.

At Global Florida Realty, we recognize the complexities of rental income reporting. Our team (with nearly 30 years of expertise in Florida real estate) can provide valuable insights into these tax matters. While we don’t offer direct tax services, we can connect you with trusted professionals who specialize in real estate taxation.

As we move forward, let’s examine the various deductible expenses associated with rental properties, which can significantly impact your overall tax liability.

Rental property owners can reduce their tax burden by leveraging available deductions. The IRS allows landlords to deduct various expenses related to owning and maintaining rental properties. These deductions optimize your investment’s financial performance.

Mortgage interest often represents one of the largest deductions for rental property owners. You can deduct home mortgage interest on the first $750,000 ($375,000 if married filing separately) of indebtedness. This includes interest on mortgages, home equity loans, and lines of credit used for rental property purposes.

Property taxes are another substantial deduction. You can deduct the full amount of property taxes paid to your local government. Recent tax law changes have capped the total state and local tax (SALT) deduction at $10,000 for personal residences. This cap doesn’t apply to rental properties, allowing you to deduct the full amount of property taxes paid on your investment properties.

The IRS distinguishes between repairs and improvements, which affects how you deduct these expenses. Repairs maintain your property in good condition and are fully deductible in the year you incur them. Examples include fixing leaky faucets, repainting, or replacing broken windows.

Improvements add value to the property or extend its life. You must capitalize and depreciate these over time. Examples include adding a new roof, renovating a kitchen, or installing central air conditioning. While you can’t deduct the full cost of improvements immediately, you can recover these costs through depreciation.

Depreciation allows you to recover the cost of business or income-producing property through deductions for depreciation. Residential rental properties typically depreciate over 27.5 years using the straight-line method. This means you can deduct a portion of your property’s value each year, even if its market value increases.

For example, if you purchased a rental property for $275,000 (excluding land value), you could potentially deduct $10,000 annually in depreciation ($275,000 ÷ 27.5 years). This deduction can significantly reduce your taxable rental income.

Land value isn’t depreciable. You’ll need to separate the value of the building from the land when calculating depreciation. Professional appraisals or tax assessments can help determine this allocation.

Other deductible expenses for rental properties include:

Try to keep meticulous records of all these expenses (including receipts and invoices) to maximize your deductions and support your claims in case of an audit.

Vacation rental ownership allows for various expense deductions, including mortgage interest, property taxes, insurance, utilities, and maintenance costs.

Rental properties count as income for tax purposes, and accurate reporting is essential. Property owners must account for various income sources, from monthly rent to retained security deposits. Proper tax planning for rental property owners provides significant benefits, including leveraging available deductions and understanding the nuances of repairs versus improvements.

The intricacies of rental property taxation often require professional guidance. Complex situations, such as mixed-use properties or substantial service provision, can complicate tax treatments. In these cases, advice from tax professionals well-versed in real estate matters proves invaluable.

At Global Florida Realty, we understand the challenges property owners face in managing their investments. Our team’s experience in the Florida market allows us to connect clients with trusted tax professionals who can provide tailored advice. Sound tax strategies play a crucial role in maximizing returns on your real estate investments.